Why are customers really leaving their banks? Not for better interest rates. Not for rewards. But for better experiences.That’s the core insight behind the latest Banking CX transformation research from Sogolytics.

A customer opens their banking app to complete a simple transaction—only to face slow loading times, confusing navigation, and unclear support options. Within minutes, frustration sets in. In today’s frictionless digital economy, that moment is all it takes to trigger a switch. Banking loyalty is no longer built on legacy trust—it is earned through consistent, seamless experiences.

This is where Banking CX transformation becomes critical. As switching barriers collapse, experience—not pricing—has emerged as the defining competitive advantage. Financial institutions are being re-evaluated daily based on usability, responsiveness, and trust.

In this context, we speak with Haris Azmi, Chief Revenue Officer at Sogolytics, whose recent research into U.S. banking customers reveals a striking shift: service quality and data security now outweigh traditional incentives like interest rates and rewards. His perspective offers a timely lens into how banks must rethink customer experience to remain relevant.

Banking CX Transformation

Q1. How do you define customer experience in the context of Banking CX transformation today?

HA: Customer experience in banking is the sum of every interaction a customer has with their institution, from checking a balance in a mobile app to resolving a dispute at a branch. What’s changed is the bar. Half of U.S. banking customers now primarily bank digitally, rarely visiting a branch. That shift means a bank’s digital experience is no longer a differentiator; it’s the floor. For CX transformation to mean something, it must extend beyond channel optimization to consistency. Our Q1 2026 research shows that 53% of consumers say their expectations are higher now than five years ago. Banks that define CX as satisfying individual touchpoints are fighting the last war. The measure that matters is whether every interaction, across every channel, reinforces or erodes trust.

Q2. What distinguishes experience-led banks from traditional product-led institutions?

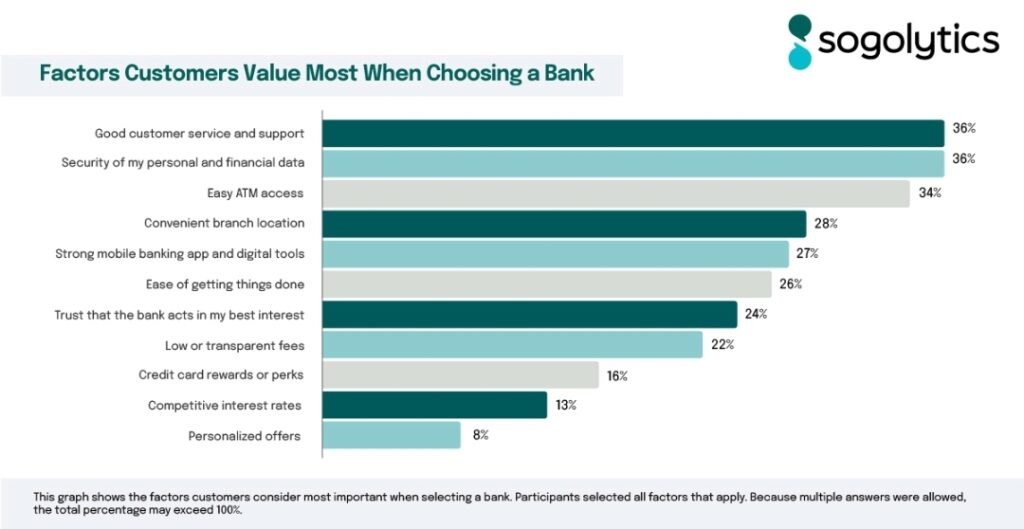

HA: Product-led institutions optimize around what they offer. Experience-led institutions optimize around how customers feel after they’ve been served. In our banking study, the top factors customers cite when choosing a bank are customer service and security, each at 36%, followed by ATM access at 34%. Competitive interest rates rank near the bottom at 13%. That’s not a fluke; it reflects a fundamental shift in how customers evaluate banks. Experience-led institutions understand this and build measurement systems to track it, act on feedback, and close the gap between what customers expect and what they receive.

Experience or Financial Benefits?

Q3. Based on your research, why are customers willing to switch banks primarily for experience rather than financial benefits?

HA: Because the financial differences between major banks are often marginal, while the experience differences are felt daily. Our data shows that roughly one third of banking customers say they would be likely or very likely to switch if another institution offered a noticeably better experience. Traditional incentives like rewards programs and personalized offers rank lowest among decision drivers. What this tells us is that customers have largely stopped expecting meaningful financial differentiation between large banks. What they do expect is ease, speed, and confidence that their bank is on their side. When those expectations are not met consistently, switching becomes rational.

Q4. How should banks structurally embed Banking CX transformation into their business strategy?

HA: It requires moving CX out of the service function and into the strategy function. Banks that treat customer experience as a program, rather than a discipline, will always be reacting to problems rather than preventing them. Structurally, this means connecting CX metrics to executive accountability, building feedback loops that surface issues before they show up in switching behavior, and measuring experience at the channel level, not just overall satisfaction. Our Q1 research found that only 34% of customers say their feedback has led to clear improvements. That number reflects an execution gap, not a data gap. Most banks are collecting feedback. Far fewer are demonstrating that it changes anything.

Leader in Digital Experience Metrics

Q5. JPMorgan Chase leads in digital experience metrics—what role do technology and platform design play in enabling this level of CX maturity?

HA: Technology creates the infrastructure; design creates the experience. JPMorgan Chase leads across ease, speed, and digital self-service in our banking study. Eighty-seven percent of their customers say mobile app tasks are easy to complete, 82% say they feel fast, and 59% say the bank’s digital tools help them accomplish tasks without needing assistance. Those numbers don’t emerge from a single feature. They reflect a sustained investment in reducing friction at every step of the customer journey. What separates mature digital experiences from the rest is not capability, it’s consistency. The best platforms do not just work; they work reliably across contexts, and they make customers feel capable.

Q6. How can banks leverage AI and analytics to better anticipate and respond to customer needs?

HA: The highest-value application of AI in banking is moving from reactive to predictive. Most banks today use AI to handle volume: routing inquiries, surfacing alerts, automating routine transactions. The next level is anticipating needs before customers articulate them. That requires connecting behavioral signals to experience outcomes and acting on them in real time. Our broader CX research shows that 55% of consumers are now willing to use automated tools for faster experiences, up from 43% last year. Customers are increasingly open to AI. The constraint is not acceptance; it is accuracy and trust. When automated features support banking needs very well, satisfaction follows. The 41% of JPMorgan customers who say their automated features do exactly that tells you what a well-implemented approach looks like.

Delivering Consistent Customer Experience

Q7. What role does internal culture play in delivering consistent customer service and support?

HA: Culture is the mechanism through which strategy becomes behavior. A bank can invest in every channel and still deliver inconsistent experiences if the people operating those channels are not aligned around the same standard of service. Our research consistently shows that branch interactions remain a meaningful part of the banking relationship, even as digital banking dominates. JPMorgan Chase leads in branch satisfaction, with 69% of their customers saying they are very satisfied with the help received from branch staff. That number does not come from scripts. It comes from an environment where staff understand what a good interaction looks like and are supported to deliver it. Culture does not guarantee great experiences, but a weak culture makes great experiences impossible to sustain.

Q8. How can banks align employee experience with Banking CX transformation goals?

HA: The connection is more direct than most organizations acknowledge. Employees who feel supported, equipped, and informed are better positioned to deliver consistent customer experiences. In financial services specifically, our State of EX 2026 data shows that 74% of employees say workplace technology has a positive impact on their work, and 55% hold a positive perception of AI. Those numbers matter because employee comfort with the tools and systems they use translates directly into the quality of their customer interactions. CX transformation that ignores how employees experience their own work is built on an unstable foundation. Aligning EX and CX goals means ensuring that the systems, training, and expectations on the employee side match what you are promising customers on the outside.

Customer Loyalty and Switching Behavior

Q9. Which CX metrics best predict customer loyalty and switching behavior in banking?

HA: From our data, the most predictive signals are effort, recommendation intent, and switching propensity. When customers report low effort to accomplish everyday banking tasks, satisfaction and loyalty follow. When that effort is high, or when digital tools fail to deliver, satisfaction erodes quickly. Recommendation scores are a lagging indicator of overall relationship health. In our banking study, JPMorgan Chase leads with 36% of customers giving a perfect recommendation score, and also shows the lowest effort ratings across channels. Those two metrics tend to move together. On the risk side, switching propensity is worth watching at the institution level. Bank of America has the highest share of customers open to switching at 45%, which is a meaningful signal about relationship fragility, even if overall satisfaction scores are acceptable.

Q10. How should banks interpret indicators like recommendation scores and satisfaction in a competitive landscape?

HA: Satisfaction and recommendation scores need to be read relative to context, not just compared to historical benchmarks. In a landscape where overall banking satisfaction is high and most customers report positive experiences, average scores can mask meaningful risk. Our data shows that roughly one third of customers across banks say they would switch for a better experience. That is not a leading indicator; it is current sentiment. Banks that see strong satisfaction scores and conclude there is no urgency are misreading the market. The relevant question is not whether your scores are good. It is whether the gap between your performance and your competition is wide enough to retain customers who are actively evaluating alternatives.

Practices Differentiate Leaders

Q11. What specific practices differentiate leaders like JPMorgan Chase in your study?

HA: JPMorgan Chase leads across every dimension we measured: ease, speed, digital self-service, branch experience, trust, overall satisfaction, and recommendation scores. The pattern that stands out is consistency. They do not lead by a dramatic margin on any single metric; they lead across all of them. That is harder to achieve than a single standout feature. It reflects investment in the fundamentals: a mobile app that works quickly and reliably, branch staff who resolve issues efficiently, and digital tools that reduce the need for assistance in the first place. The 89% of JPMorgan customers who express confidence in their bank’s digital tools is the kind of number that builds durable loyalty.

Q12. Bank of America shows higher switching risk—what practical steps should such institutions take to close the experience gap?

HA: Start with the metrics that show the most distance from competitors. Bank of America ranks fourth or fifth in mobile app ease, website ease, and digital self-service, and has the highest switching intent in the study at 45%. That combination points to a digital experience that is not keeping pace with customer expectations. The practical path forward is not a platform overhaul. It is identifying the specific friction points that generate the most dissatisfaction and addressing them systematically. Our broader CX research shows that long wait times and poor communication are the top drivers of negative experiences. Even incremental improvements in resolution speed and digital clarity reduce switching intent in ways that customers notice and reward.

Banking CX Transformation

Q13. How do you see Banking CX transformation evolving over the next 3–5 years?

HA: Three forces will drive the next phase. First, the baseline will continue to rise. As JPMorgan Chase and other leaders normalize 85 to 90% satisfaction on digital channels, mid-tier performers will face increasing pressure to close the gap or accept higher attrition. Second, AI will move from a support function to a core experience layer. Banks that figure out how to use AI to anticipate needs, not just handle volume, will create genuine differentiation. Third, trust will become a harder-earned asset. Our Q1 CX research shows customers are placing greater weight on data protection and transparency, with 43% saying companies should be more transparent about data use. Banks that treat customer data as a relationship resource rather than an operational byproduct will have a structural advantage.

Q14. What emerging trends will redefine customer expectations in financial services?

HA: Three trends stand out. First, the convergence of experience and security. Our data shows security and customer service are tied at 36% as the top decision drivers. As cyber threats become more visible in the news, customers will increasingly evaluate banks on their ability to protect them, not just serve them. Second, the normalization of AI-assisted banking. Fifty-five percent of consumers are now willing to use automated tools for faster experiences. That share will grow. The banks that deploy AI in ways that are fast, accurate, and transparent will benefit; those that use it to deflect customers rather than assist them will not. Third, the expectation of follow-through on feedback. Customers are sharing feedback more than ever, but only 34% say their input leads to visible changes. Closing that loop will become a competitive differentiator.

Advise Banking Leaders

Q15. If you had to advise banking leaders on one decisive shift they must make today to stay relevant in the era of Banking CX transformation, what would it be?

HA: Treat customer experience data as a business intelligence function, not a reporting function. Most banks measure satisfaction. Very few use that measurement to drive decisions at the speed customers expect. About one third of customers are already willing to switch for a better experience. That window is not closing; it is widening. The institutions that will remain relevant are those that can close the loop between what customers tell them and what changes as a result. That requires infrastructure, accountability, and leadership that treats CX as a strategic input, not a quarterly scorecard.

Reader Takeaways

Experience—not pricing—is now the primary driver of banking loyalty

Digital usability and service responsiveness are critical CX differentiators

Trust and security are foundational to customer retention

Continuous feedback and benchmarking are essential for CX leadership

Interview Closing

As banking continues its shift toward experience-led differentiation, one message comes through with clarity: customers are no longer comparing banks—they are comparing experiences. In a world where switching is effortless, loyalty is fragile, and expectations are continuously reset by digital leaders across industries, Banking CX transformation has become both a strategic imperative and a competitive necessity.

The insights shared by Haris Azmi reinforce a critical inflection point for financial institutions. Experience is no longer a supporting function—it is the product. From mobile usability to trust in data security, from responsive service to seamless journeys, every interaction now shapes brand perception and retention. Institutions that fail to operationalize Banking CX transformation risk not just losing customers, but losing relevance.

Looking ahead, the path forward demands more than incremental improvements. It requires a deliberate rethinking of how banks listen, design, and deliver value at every touchpoint. The leaders in this space will be those who embed Banking CX transformation into their cultural DNA—aligning technology, people, and strategy around a singular goal: making banking effortless, intuitive, and trustworthy.

For CX leaders, the takeaway is unmistakable—Banking CX transformation is no longer about staying ahead. It is about staying in the game.