The head of retail banking stared at the dashboard.

Loan approvals were stuck, fraud alerts were spiking, and customer NPS had dropped three points in a quarter. Everyone blamed something different: legacy systems, manual checks, compliance cycles, or “AI that never made it past the pilot.”

This is where AI-native banking operations are quietly redefining how CX, risk, and efficiency come together.

What Is AI-Native Banking Operations and Why CX Leaders Should Care?

AI-native banking operations use automation, analytics, and GenAI to redesign workflows end-to-end, not just speed up existing manual steps. CX leaders should care because it directly impacts decision speed, cost-to-serve, compliance, and experience across lending, payments, and servicing.

Instead of throwing more people at broken processes, AI-native operations combine:

- Transaction processing, servicing, and risk in unified workflows

- Automation plus human expertise, orchestrated by platforms

- Continuous learning from data and interactions, not one-off projects

In banking, this is no longer theory.

Independent analyst recognitions now highlight which providers are actually doing this at scale, not just pitching slideware.

How Are Analysts Redefining “Good” in Banking Operations?

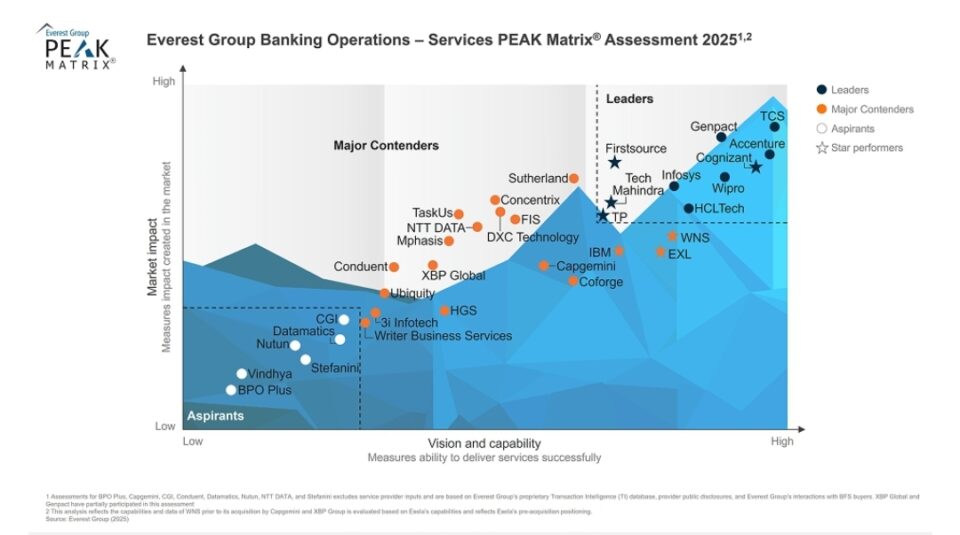

Industry analyst firms now evaluate banking operations on AI maturity, domain depth, and real outcomes, not just FTE counts and SLAs. Recent assessments place Firstsource in the Leader band for both banking operations and GenAI-led automation.

Everest Group’s Banking Operations – Services PEAK Matrix Assessment 2025:

- Positions Firstsource as a Leader and Star Performer in banking operations services

- Highlights integrated support across cards, lending, collections, servicing, and financial crime

- Emphasizes a transformation-led delivery model and a digital-first operating approach

NelsonHall’s 2025 NEAT for GenAI & Process Automation in Banking:

- Recognizes Firstsource as a Leader across both operations services and process automation services

- Calls out deep lending and mortgage expertise and tailored solutions for regional and local banks

- Notes a scaled GenAI workforce and a clear agentic AI strategy, focusing on high-value processes

For CX/EX leaders, these recognitions matter because they shift the benchmark.

“Good operations” now means AI-native, domain-deep, and outcome-driven, not just low-cost and compliant.

What Makes Firstsource’s Approach Different for CX and Operations?

Firstsource’s model blends UnBPO™, BPaaS, and agentic AI to move clients from pilots to production-grade AI in banking workflows. This matters for CX because it touches real customer journeys: onboarding, servicing, collections, and dispute resolution.

Key building blocks include:

- UnBPO™: A differentiated approach that reimagines outsourcing around platforms, data, and domain-led teams, not just labor arbitrage.

- BPaaS: Banking processes delivered as a service with embedded automation, analytics, and AI, so banks consume outcomes rather than manage every process detail.

- Agentic AI and platforms:

- relAI™ for workflow modernization and guided processing

- AI Coach and QC Copilot to support agents and quality teams

- AI on images and video for cybersecurity and fraud use cases

Leaders at Firstsource frame this shift clearly: the move is from labor-centric models to AI-native, outcome-driven operations. Analyst commentary reinforces that this is backed by investments in platforms, data, analytics, and workflow orchestration, not just point tools.

How Does AI-Native Banking Fix Siloed Journeys and Fragmented CX?

AI-native banking operations attack the root causes of journey fragmentation: disconnected systems, manual checks, and channel silos. By treating banking workflows as integrated journeys, rather than isolated tasks, providers can redesign the experience around outcomes.

Consider three high-impact areas:

- Lending journeys

- Pre-qualification to disbursal runs on unified workflows that blend credit data, income verification, and fraud checks.

- GenAI and automation reduce manual document review, while decision engines keep risk policies consistent.

- Payments and servicing

- Disputes, chargebacks, and inquiries route through orchestrated workflows that guide agents and bots.

- AI Coach can suggest next best actions, while QC Copilot helps supervisors scale quality reviews.

- Fraud and financial crime

- Integrated support across cards, collections, and financial crime avoids duplicated investigations and conflicting decisions.

- AI models and domain teams work together to reduce false positives and cycle times.

The result is fewer handoffs, faster decisions, and more consistent experiences.

CX leaders see this in shorter onboarding times, lower abandonment, and improved NPS on complex journeys like loans and disputes.

What Framework Can CX Leaders Use to Evaluate AI-Native Operations?

CX and EX leaders need a practical lens to assess banking operations partners and internal capabilities. A simple 4D framework helps structure the conversation.

1. Domain

Ask: Does the provider have inch-wide, mile-deep expertise in specific banking processes, or are they generalists?

Look for:

- Specialization in lending, cards, collections, fraud, or servicing

- Track record with regional and local institutions, not just global majors

- Domain-led platforms and playbooks, not generic BPM tooling

2. Design

Ask: Are workflows designed around customer and employee experience, or just compliance and cost?

Evaluate:

- End-to-end journey mapping for onboarding, servicing, and collections

- Embedded controls for compliance and risk, versus bolt-on checks

- Use of guided processing and next-best-actions for frontline teams

3. Data & Decisions

Ask: How does the operation use data and AI to make better, faster decisions?

Probe:

- Role of AI in triage, classification, recommendations, and risk scoring

- Continuous learning from outcomes and feedback loops

- Ability to apply GenAI to documents, images, and multimedia for real banking use cases

4. Delivery

Ask: Is the delivery model flexible, AI-native, and geared to outcomes, not just FTEs?

Check:

- BPaaS offerings with clear SLAs on time-to-yes, resolution rates, or fraud catch rates

- Scaled GenAI workforce and engineering capabilities, not just operations talent

- Proven track record moving from pilots to production in months, not years

Sample Evaluation Table for CX Leaders

| Dimension | What “Legacy” Looks Like | What “AI-Native” Looks Like |

|---|---|---|

| Domain | Generic BFS coverage only | Deep focus on lending, cards, fraud, and servicing with tailored plays. |

| Design | Step-level optimization | Journey-level workflows across onboarding, servicing, and collections. |

| Data | Basic reporting | AI, GenAI, and analytics embedded in decisions and routing. |

| Delivery | FTE-based outsourcing | BPaaS, UnBPO™, and outcome-based constructs. |

What Are Common Pitfalls CX Teams Face with GenAI in Banking Operations?

Most CX and operations teams stumble not on AI models, but on change, integration, and scope.

Common pitfalls include:

- “Pilot paralysis”

- Running many proofs of concept with no clear path to scale.

- Focusing on narrow use cases with low business impact.

- Siloed AI initiatives

- Separate projects in fraud, collections, and CX, with little shared data or learnings.

- Conflicting KPIs across teams and vendors.

- Overlooking EX

- Adding AI tools without redesigning agent workflows and coaching models.

- Failing to equip frontline teams with training and context.

- Compliance as an afterthought

- Building GenAI use cases, then retrofitting controls and documentation.

- Missing stakeholder alignment with risk, legal, and audit from day one.

Leaders who avoid these pitfalls usually partner with providers that combine AI, operations depth, and a structured change approach.

Key Insights for CX and EX Leaders

- Analyst-recognized leaders in banking operations are now defined by AI-native, outcome-focused models, not just low cost.

- Platforms such as relAI™, plus tools like AI Coach and QC Copilot, show how AI can support both customer journeys and frontline experience.

- UnBPO™ and BPaaS structures help banks consume outcomes while keeping compliance and risk embedded in the operating model.

- Dual recognitions from major analyst firms signal that scalable, production-grade GenAI in banking is already here, not a future experiment.

FAQ: AI-Native Banking Operations and CX

1. How is AI-native banking different from traditional outsourcing?

AI-native banking operations integrate AI, automation, and analytics into the core of processes, while traditional outsourcing mainly shifts work to external teams without redesigning workflows or decisions.

2. Can smaller or regional banks benefit, or is this only for global players?

Regional and local institutions are a key focus, with tailored solutions for lending, mortgage, and servicing, plus BPaaS models that reduce upfront investment.

3. Where should CX leaders start if journeys are heavily fragmented?

Start with one high-impact journey—often lending or collections—and map end-to-end pain points, then partner to redesign using AI-native workflows and clear outcome metrics.

4. How does GenAI improve agent experience in banking operations?

GenAI supports agents through guided responses, document summarization, case insights, and quality coaching tools, improving speed, consistency, and learning without replacing human judgment.

5. What risks should CX leaders watch when scaling GenAI in operations?

Key risks include model bias, explainability gaps, data privacy, and control breakdowns, which is why leading providers stress secure, production-grade AI with embedded governance.

6. How can CXQuest content support teams on this journey?

CXQuest’s strategy and technology hubs provide playbooks on AI-enabled CX, journey orchestration, and EX design, helping leaders align partner choices with internal capability-building.

Actionable Takeaways for CX and EX Leaders

- Map one end-to-end banking journey (e.g., loan origination) and identify three friction points where automation and AI could change outcomes.

- Use the 4D framework (Domain, Design, Data & Decisions, Delivery) to evaluate your current operations and external partners.

- Prioritize partners that show independent analyst validation in both operations and GenAI, not just one or the other.

- Design a joint “from pilot to production” roadmap with clear timeframes, KPIs, and risk controls for your first AI-native journey.

- Embed EX into every AI initiative: define how tools like AI Coach or copilots will change agent workflows, coaching, and quality.

- Align with risk, legal, and compliance upfront to codify GenAI policies, controls, and audit trails across workflows.

- Create a unified CX–Risk–Operations steering group to oversee AI-native transformation in banking journeys.

- Use CXQuest content and internal communities of practice to share wins, patterns, and playbooks as you scale AI-native banking operations.