From Batch to Brilliant: How RBI’s Cheque Revolution is Redefining Banking Customer Experience

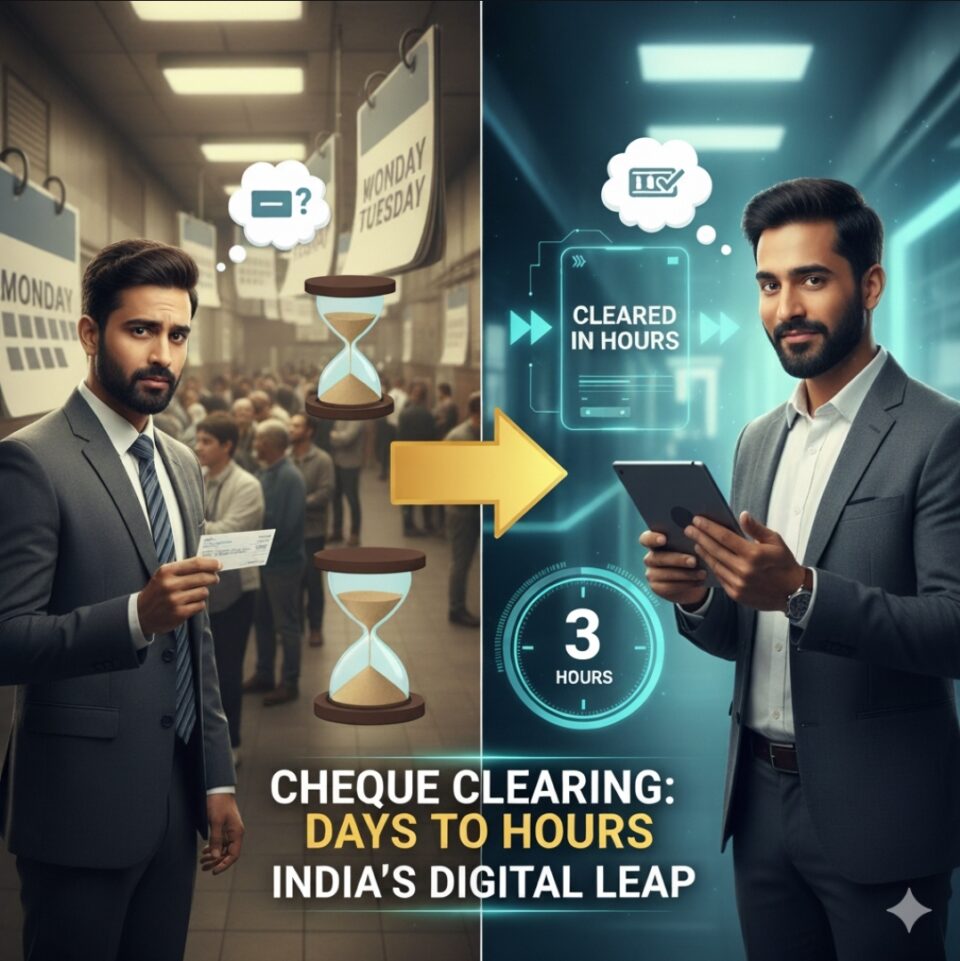

Picture this: you deposit a cheque on Monday morning, eagerly waiting for the funds to clear, only to watch two precious business days tick by before the money finally appears in your account. For countless banking customers across India, this familiar Cheque Clearing frustration has been the norm for decades. But what if that wait time could shrink from days to mere hours?

The Reserve Bank of India’s groundbreaking shift to continuous cheque clearing, launched on October 4, 2025, represents more than just a technical upgrade—it’s a fundamental reimagining of what modern banking customer experience should deliver. This transformation from batch processing to real-time settlement signals a broader evolution in how financial institutions must balance operational efficiency with customer-centric service delivery.

The Dawn of Same-Day Banking Reality

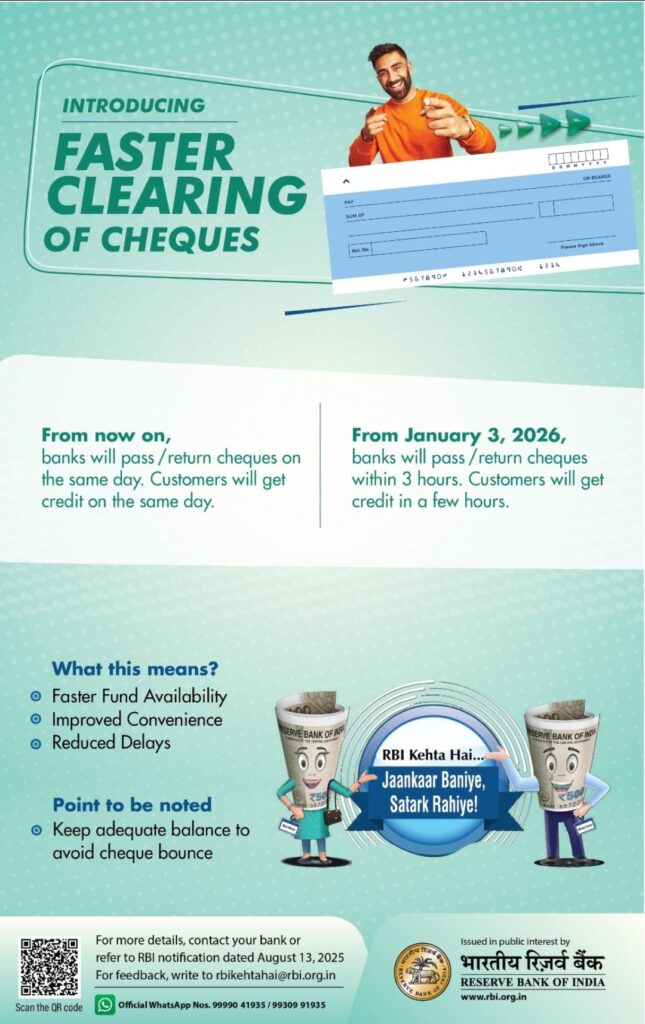

The traditional cheque clearing system operated like clockwork—predictable, methodical, but painfully slow. Banks processed cheques in fixed batches once or twice daily, creating bottlenecks that turned simple transactions into multi-day ordeals. Under the new continuous clearing framework, cheques deposited between 10 AM and 4 PM are scanned and transmitted instantly, with hourly settlements beginning at 11 AM.

This isn’t merely about speed improvements. Banks now have strict confirmation windows: Phase 1 requires responses by 7 PM, while Phase 2, beginning January 3, 2026, compresses this timeline to just three hours. If a bank fails to respond within these timeframes, the cheque automatically receives approval and enters settlement.

The customer impact is immediate and tangible. Funds that previously took one to two business days now reach accounts within hours, transforming cheque transactions from obstacles into seamless financial tools. This acceleration brings cheque processing speed in line with electronic payment systems like NEFT and RTGS, finally delivering the consistency customers expect across all banking channels.

Beyond Technology: The Human Element in Digital Transformation

However, early implementation challenges reveal a critical truth about banking transformation: technology alone cannot deliver superior customer experience. Reports indicate that several banks encountered difficulties during the initial rollout, with staff struggling to adapt to new processes and technical glitches affecting cheque quality and scanning consistency.

Customer complaints about delays and inconsistent service highlight a fundamental gap between technological capability and operational readiness. Bank employees, suddenly thrust into real-time processing requirements, faced challenges in scanning procedures, system integration, and troubleshooting—skills that require comprehensive training and ongoing support.

This situation underscores a broader principle in banking customer experience: successful transformation demands equal investment in human capital alongside technological infrastructure. Banks that prioritize employee training, establish clear escalation procedures, and maintain robust support systems during transition periods create the foundation for sustained service excellence.

Operational Excellence Through Employee Empowerment

The cheque clearing transformation offers valuable lessons for banking leaders seeking to enhance customer experience across all touchpoints. Research indicates that emotionally intelligent bank employees deliver significantly better customer service outcomes, building stronger relationships and resolving issues more effectively.

Modern customer service training programs increasingly emphasize soft skills development alongside technical competency. Banks implementing comprehensive training initiatives report measurable improvements in customer satisfaction scores, reduced complaint volumes, and enhanced employee confidence when handling complex situations.

Cross-training initiatives that prepare staff to manage multiple customer scenarios prove particularly effective. When employees understand both traditional processes and new digital workflows, they can guide customers seamlessly through transitions while maintaining service quality standards.

Training programs focusing on active listening, empathy, and conflict resolution equip frontline staff with tools to transform potentially negative experiences into positive customer interactions. These skills become especially critical during periods of system change, when customers may feel confused or frustrated by new procedures.

The Experience Economy: Branches as Advisory Centers

The cheque clearing revolution reflects a broader shift in banking strategy—the evolution from transaction-focused operations to experience-centered service delivery. Leading banks are transforming physical branches from teller-line environments into advisory centers where technology enhances rather than replaces human interaction.

This transformation requires fundamental changes in staff roles and responsibilities. Employees must develop consultative skills, becoming financial guides who help customers navigate both digital and traditional banking options. Success in this environment depends on comprehensive product knowledge, emotional intelligence, and the ability to translate complex financial concepts into accessible guidance.

Banks investing in branch transformation report that customers increasingly value personalized advice and trusted human connections, even as digital adoption accelerates. The key lies in creating seamless integration between digital efficiency and human expertise, allowing customers to access both self-service convenience and professional guidance as needed.

Community integration becomes a crucial differentiator, with successful branches serving as local financial education hubs that build lasting relationships beyond individual transactions. These initiatives strengthen customer loyalty while establishing banks as trusted community partners.

Process Automation: Balancing Efficiency with Human Touch

The continuous cheque clearing system demonstrates how process automation can enhance rather than diminish customer experience when implemented thoughtfully. Automated workflows eliminate manual bottlenecks while ensuring consistent service delivery across all customer touchpoints.

Successful banking automation initiatives focus on eliminating repetitive tasks that frustrate both customers and employees, freeing staff to concentrate on high-value advisory services. Customer onboarding, loan processing, and routine inquiries benefit significantly from automated workflows that reduce processing times without sacrificing accuracy or compliance standards.

However, automation strategies must preserve opportunities for human intervention when customers need personalized assistance. The most effective implementations create hybrid models where technology handles routine processes while maintaining easy access to knowledgeable staff for complex situations.

Banks achieving optimal results from automation invest heavily in staff training that helps employees understand how automated systems work and when human intervention adds value. This knowledge enables staff to troubleshoot issues quickly and guide customers effectively through both automated and manual processes.

Cultural Transformation: Building Customer-Centric Organizations

The technical success of continuous cheque clearing ultimately depends on broader cultural transformation within banking organizations. Customer-centric cultures prioritize service excellence at every level, from executive decision-making to frontline interactions.

Organizational culture shapes how employees respond to challenges during transformation periods. Banks with strong customer-first cultures demonstrate greater resilience when technical issues arise, with staff proactively communicating with customers and finding alternative solutions to maintain service quality.

Leadership commitment to customer experience excellence creates ripple effects throughout organizations. When executives model customer-focused behavior and invest in employee development, frontline staff feel empowered to go beyond basic transaction processing to deliver memorable service experiences.

Feedback systems that capture both customer and employee perspectives enable continuous improvement in service delivery. Banks that actively solicit input from both groups and implement meaningful changes demonstrate genuine commitment to experience excellence.

Measuring Success: KPIs That Matter

Effective customer experience measurement extends beyond traditional metrics like transaction volume or processing speed. Leading banks track comprehensive indicators including customer satisfaction scores, first-call resolution rates, employee engagement levels, and complaint resolution timeframes.

Digital adoption rates provide valuable insights into customer preferences and areas requiring additional support. Banks monitoring these metrics can identify customers who might benefit from additional training or assistance with new processes.

Employee confidence and competency metrics reveal the effectiveness of training programs and highlight areas needing additional investment. Regular skills assessments ensure staff capabilities keep pace with evolving customer expectations and technological requirements.

Customer effort scores measure how easy or difficult customers find various banking processes. These metrics often reveal disconnect between intended process improvements and actual customer experiences, highlighting opportunities for further refinement.

Strategic Recommendations for Banking Leaders

Banking executives seeking to maximize the customer experience benefits of operational transformations should prioritize comprehensive change management that addresses both technological and human factors simultaneously. Training programs must begin well before system launches and continue through transition periods with regular skill assessments and refresher sessions.

Communication strategies should emphasize benefits to customers while acknowledging potential temporary inconveniences during adjustment periods. Transparent, proactive communication builds customer confidence and reduces frustration when issues arise.

Investment in employee development creates competitive advantages that extend far beyond individual transformation initiatives. Banks that consistently invest in staff training, emotional intelligence development, and customer service skills build resilient organizations capable of adapting to future changes while maintaining service excellence.

Technology implementations should include robust fallback procedures and manual override capabilities to ensure service continuity when automated systems encounter issues. Staff must understand these procedures thoroughly and feel confident implementing them when necessary.

Continuous monitoring and rapid response capabilities enable banks to identify and address issues before they significantly impact customer experience. Real-time feedback systems and escalation procedures ensure problems receive prompt attention and resolution.

The RBI’s continuous cheque clearing initiative represents more than operational efficiency improvement—it exemplifies how thoughtful technology implementation, combined with strategic human capital investment, can transform customer experience across entire banking ecosystems. Success requires equal attention to technological capability and human readiness, creating organizations that deliver consistently excellent service regardless of the challenges they encounter.